Have you ever thought that even after saving money regularly, your bank balance is not actually growing in real terms? This happens because of inflation.

For example:

Today you can buy groceries for ₹1000.

After 10 years, the same groceries may cost ₹1800–₹2000.

This means that if your money is lying idle in a savings account, its purchasing power is continuously decreasing. So the question arises:

How can a common salaried person grow their money without taking huge risks?

The answer is — Systematic Investment Plan (SIP).

What is SIP in Mutual Funds?

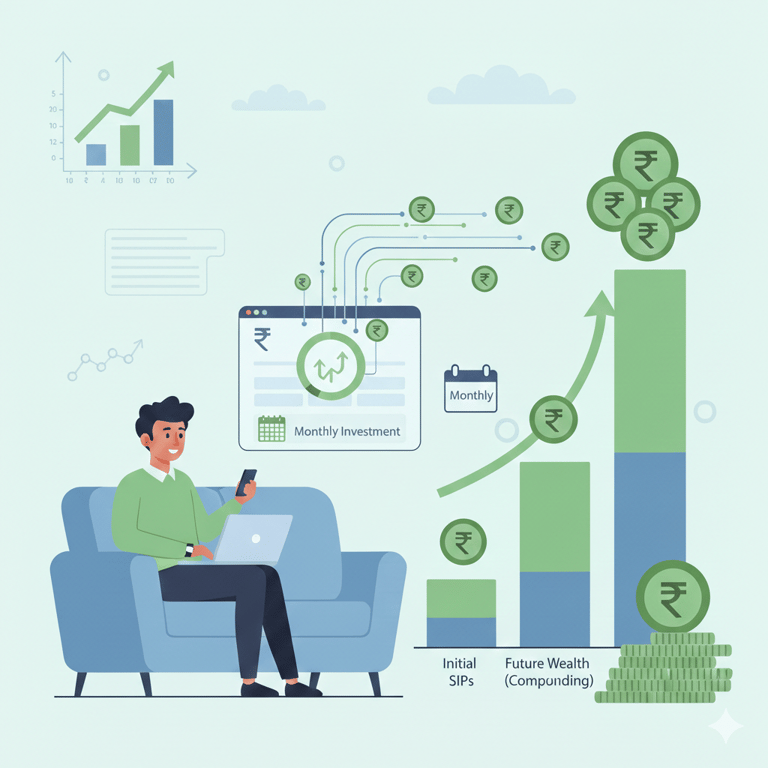

SIP (Systematic Investment Plan) is a method of investing a fixed amount of money regularly in mutual funds. Instead of investing a big amount at once, you invest a small amount every month.

For example:

₹500 per month

₹1000 per month

₹2000 per month

₹5000 per month

SIP allows you to invest according to your income and financial capacity. Even a student or a beginner investor can start SIP.

Real Life Example of SIP

Let us understand SIP with a very simple example.

Suppose you spend:

₹100 daily on tea, snacks, or online food ordering. If you save this ₹100 daily and invest:

₹3000 per month through SIP

for 15 years

at an average return of 12%

Then:

Your Total Investment = ₹5,40,000

Your Expected Returns = ₹9,73,000 approx

Your Total Wealth = ₹15,00,000 approx

So by simply controlling small daily expenses, you can create wealth of ₹15 lakh in the long term.

How SIP Works?

When you invest through SIP:

You invest a fixed amount every month.

Mutual funds buy units on your behalf.

When market is low → you get more units.

When market is high → you get fewer units.

This concept is known as Rupee Cost Averaging. Over time, this helps in reducing market risk.

Power of Compounding in SIP

Compounding means earning returns on your invested amount as well as on the returns generated earlier.

Example:

Person A starts SIP at age 25

Person B starts SIP at age 35

Both invest ₹3000 per month.

Even though Person A invests only 10 years more than Person B, his final wealth may be almost double due to the power of compounding.

This is why financial experts say:

Start early, invest regularly.

SIP vs Lumpsum Investment

SIP Investment

✔ Invest a large amount at once

✔ Suitable for experienced investors

✔ Higher market risk

✔ Requires proper market timing

✔ Good during market downturn

✔ Ideal for investors with surplus funds

Lumpsum Investment

✔ Invest fixed amount every month

✔ Suitable for beginners

✔ Lower market risk

✔ No need to time the market

✔ Helps in disciplined investment

✔ Ideal for salaried individuals

What is Step-Up SIP?

Step-Up SIP allows you to increase your SIP amount every year as your salary increases.

Example:

Year 1 – ₹2000/month

Year 2 – ₹3000/month

Year 3 – ₹4000/month

This helps you build a much bigger investment corpus without feeling financial pressure initially.

You can also calculate Step-Up SIP returns using our SIP Calculator.

Who Should Invest in SIP?

SIP is suitable for:

Salaried Employees

Government Employees

Students

First Time Investors

Long Term Wealth Creators

Retirement Planners

Benefits of SIP Investment

✔ Disciplined Investment

✔ Small Investment Amount

✔ Power of Compounding

✔ Market Risk Reduction

✔ No Need to Time Market

✔ Long Term Wealth Creation

Conclusion

SIP is one of the easiest and safest ways to start investing in mutual funds. You do not need a huge amount of money to begin your investment journey. Even a small monthly investment can create a large financial corpus in the long run.

The key is:

Start early

Invest regularly

Stay invested for long term

Use our SIP Calculator to estimate your future returns and start your investment journey today.